What is a Spot Rate Yield Curve?

The spot rate yield curve is a graphical representation that shows the relationship between spot rates (yields of zero-coupon bonds) and their maturities. It's an essential concept in bond valuation and risk management, helping investors understand the time value of money over different periods.

The Bootstrapping Method

One common method to construct the spot rate curve is bootstrapping. This technique uses the yields of existing Treasury securities to determine a series of spot rates. Essentially, we start with the shortest-term rates and sequentially build up to longer-term rates.

Implementing in Python

To demonstrate, we'll use Python with libraries like NumPy and Matplotlib. We’ll also use numpy_financial for financial calculations. Here's a step-by-step guide:

Step 1: Prepare Your Environment

First, ensure you have Python installed. Then, install necessary libraries:

pip install numpy matplotlib numpy-financial

Step 2: Define Your Data

We begin with sample bond data. Each bond has a maturity, annual coupon rate, and market price.

bonds = [

['6-month zero-coupon bond', 0.5, 0, 99.5],

['1-year coupon bond', 1, 2, 99.8],

['1.5-year coupon bond', 1.5, 2.5, 100.1],

['2-year coupon bond', 2, 3, 100.5]

]

Step 3: Calculate Zero-Coupon Yield

For zero-coupon bonds, the yield is straightforward to calculate:

def zero_coupon_yield(price, maturity):

return (100 / price) ** (1 / maturity) - 1

Step 4: Bootstrap the Yield Curve

Now, let’s use bootstrapping to calculate the spot rates:

import numpy_financial as npf

import numpy as np

def bootstrap_yield_curve(bonds):

spot_rates = np.zeros(len(bonds))

for i, bond in enumerate(bonds):

name, maturity, coupon_rate, price = bond

cash_flows = np.zeros(int(maturity * 2))

if coupon_rate == 0:

spot_rate = zero_coupon_yield(price, maturity)

spot_rates[i] = spot_rate

continue

semi_annual_coupon = coupon_rate / 2

cash_flows[:] = semi_annual_coupon

cash_flows[-1] += 100

discounted_npv = 0

for j in range(len(cash_flows)):

if spot_rates[j] != 0:

discounted_npv += cash_flows[j] / (1 + spot_rates[j] / 2) ** (j / 2)

adjusted_initial_investment = -1 * (price - discounted_npv)

adjusted_cash_flows = [adjusted_initial_investment] + cash_flows.tolist()

irr = npf.irr(adjusted_cash_flows) * 2

spot_rates[i] = irr

return spot_rates

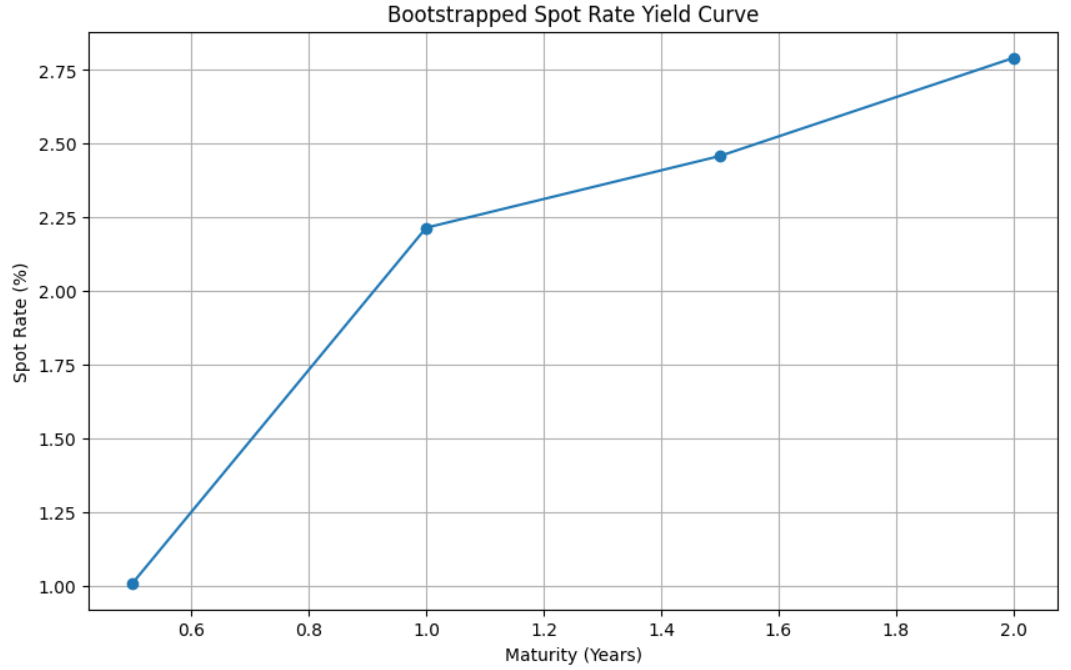

Step 5: Plot the Yield Curve

Finally, visualize the yield curve using Matplotlib:

import matplotlib.pyplot as plt

spot_rates = bootstrap_yield_curve(bonds)

plt.figure(figsize=(10, 6))

plt.plot([bond[1] for bond in bonds], spot_rates * 100, marker='o')

plt.title('Bootstrapped Spot Rate Yield Curve')

plt.xlabel('Maturity (Years)')

plt.ylabel('Spot Rate (%)')

plt.grid(True)

plt.show()

Conclusion

Building a spot rate yield curve is an essential skill in finance. This Python approach offers a practical way to understand market expectations for future interest rates. By mastering these techniques, you can gain valuable insights into bond valuation and the overall interest rate environment.